It has a variety of meanings for many people. But for me, money is just a tool to satisfy our needs and wants. My retirement goal is to stay away as far as I can from something that required money. You need to ask yourself, what money can satisfy your needs and wants? To me, my need is food. I don’t buy much clothes. I don’t buy much shoes, or bags. It’s foods, water bill, electricity bills, internet bills and a house I can call a home.

I want to retire earlier than compulsory age. I want to have a living where I don’t need to worry about bills, mortgages, and foods. my focus for retirement is to go back to basic life and needs. I want to be away from massive traffic jammed. I want to be away from toxic circle friends and families. I just want to be alive and enjoying each my day n seconds, glorifying life surrounding me. I had enough of this fake world and getting back to real purpose or living.

I set my target, to retire in the next 10 years, insya Allah.

Wow, it’s been 10 months since I updated my blog due to workload and stress. Finally, I’m freedom from Corporate World! haha, temporarily 😃

I was thinking, due to economy not stable etc, our daily expensive increase significantly lately. I know I need to do some side income, because daily life these days becoming soo expensive. I’m still survive, because of my minimalist living. But I want more than enough so that I can help those who need it, especially my families.

I’ve seen in front of my eyes how people who used to have millions in their account on surviving mode now. In my country, Malaysia, most people are working in Corporate Company, having EPF (Employees Provident Fund) saved monthly with free contributions from employer, monthly. But, I saw when they reached 55 years old and finished their saving money even before they reached 60. It’s stipulated in my mind that I still need to work even though I reached a mature age of 55 years old to take out my money.

Here is the thing on what usually happened, when someone reached 55 years old, most scammer can “smell” the new money. So, mostly people will fall for scammers. Well, I don’t wanna be such. I wanna build my own business right now, so by 55 years old, it can run itself with minimal supervision.

If you wanna get into business in Malaysia, you need to register SSM (Suruhanjaya Syarikat Malaysia) and choose an appropriate type of business. Well, it was not a smooth process for me, but eventually I managed to get my SSM certificate. Yay!!

So, here we go, bismillah to start my business.

pssstt, well, I had eventually finished renovating my new home. Will share in the next blog on my new renovated home and share some tips on how to manage new house renovation from the beginning. 🥰

I think it’s not too late yet to wish ALL of you, A Happy New Year!!!!

This year is a huge year for me as I’d accomplished most of the things that I want in my life. Wee!! 🥳

It’s been 7 years since I was becoming a minimalist. Below are things I had achieved throughout my journey 🥰

Things I’ve achieved by being a minimalist for 7 years:

More space for my home: I have sold and donated a lot of my things such as dresses, aquariums, exercise tools, etc. I just recently shifted to my a new home which already has a gym downstairs. So I won’t need boxing glove, boxing wraps, boxing knee pads, barbell etc.

More savings for mental happiness: When I stop buying clutters, I have some enough money to go to spas, hotels, and resorts. Recently there are a lot of websites which you ca have a cheaper price for entrance, hotel rooms, theme parks. Mental health is as important as physical health too. By being a minimalist, I’m morefocusedg on balancing both my physical and mental health.

Career goal achieved: This is not easy things to have, but I combined with my faith that to achieve a good environment, good colleagues and bosses and achieving my desire salary. I’m successfully balancing both desire salary with good environment by end of 2024. Alhamdulillah, praise to God. 🤲

More savings for other property: Well, I have 2 properties now. One of it I rent it out, and another one I’m staying with right now. initially, I didn’t plan to have 2 properties. Luckily, support by our government before, in the year 2021, I managed to get another one property. I was thinking this as backup retirement plan when the retirement money finished, so I have property to rent it out. It’s not easy if you need to repair on structure such leaking pipe, leaking bathroom etc. I’m trying to get rid of one property, but unfortunately, I’m still not success. So, I just rent it and be my backup plan. It’s not urgent to sell too, so I just keep the 1st property as a backup plan.

More savings for additional retirement plan : Yes, I’m buying another insurance just cover the remaining years, coz for the 1st propert, my loan was for 35 years, however the insurance only cover for 30 years. The second property loan was 35 years, and insurance just cover for 20 years. There is a huge gap and I just buy 1 insurance to cover the missed gap 😃. Other than this, I’m having another insurance which is the maturity age of 70 years old. I still thinking the best way for retirement plan other than the KWSP funds. I don’t think KWSP is enough for a retirement plan due to high raise inflation.

Focusing on retirement plan: Other than mandatory fund KWSP, I wanna diverse more funds for retirement savings. I have seen, most retirees will go broke after 10 years of retirement. The savings need to beat the high inflation to these days’ economy.

In term of financial, currently, I’m still recovering from renovation my house and insya Allah in the next 1 or 1.5 years,I will recover my finances fully and have a positive cashflow with cash in my hands.

I will share in the next post regarding how I manage my home renovation without being broke. hahaha!! It might be helpful for those in the mid of renovation your houses. Took me several months to plan out my renovation and being a main contractor to my own house.

When talking about minimalism, it’s not only about your space. It’s about lifestyle, including your space, your financial goals, your relationship. It’s about how you let go of those unnecessary and keep the mandatory that always be your goal. It’s about setting up your life goals. Minimalist have various definitions towards each of people, but for me it’s lifestyle and life goals.

I’ve started being a minimalist since 2018, to be honest the most hardly to do is to minimalist my wardrobe and cables. I’ve decluttered my space, decluttered my relationship, decluttered my circle friendship, minimizing my expenses and maximizing investment and saving. I really enjoyed the journey.

Today, I’m about to minimize my “bad debt” and transferring it to a good debt. The only “bad debt” I have now is my credit card which I’m fighting for quite so long. Today, I’m about to refinance my 1st home, and clearing all my credit card and have some cash in hand for me to build my positive cashflow – Debit Card.

Waiting in a line, my turn!! 😃

There is a lot of impact and consequences I’ve checked and put into consideration, like how much difference I need to bare, and what about insurance, how many years the new insurance will cover, is it enough until I’m at least by the age of 60/70? I’m not dare to take fewer years of insurance, so the original insurance was to cover 35 years, I’m checking for 30 years for the new insurance. Oh, by the way, the most important thing is the property has tenants and the cost can cover my whole bank now plus some little extra. By calculating everything, I saved monthly RM 1.2k!! Wee!!! Plus, my credit card settled and I have some cash in hand. So, I’m now need to think carefully what I shall do with the little money I have in hand.

Next, my target is to manage a debit card for replacing a credit card. Yay!! I was so happy as I’ve found the solution to declutter bad debt. After I’m done building positive cashf. Next, xt I’m gonna think a way on how to set goal for my retirement day!! Hey!! It’s not too earl to think about when you are nearly , okay? Nay or Yay!! 😃

Just wanna share my experience on how am I from negative cashflow to positive cashflow and can save some for investment.

First thing first, I think from my previous post, I did mentioned the rules of 50:30:20. So, to spend on monthly expenses of 50% of your salary, 30% is for self reward and 20% for future investment. Yes, this is just a fundamental for you to force yourself to save some money.

What I did was, I played the percentage by lowering my daily expenses, and putting more percentage on my investment. From 50:30:20, I goes to 40:30:30.

I strive to get rid of my monthly commitment, lowering my self indulgence rewards and chip in more to investment. Now, I found something that I can combined my self indulgence rewards and my future investment together making it 60% out of total monthly salary. Wee!! find your self reward which can make investment too for future. ❤

Hey, what’s up everyone? Hope you are all well and in a peace of mind. Insya Allah ❤

It’s been frequently hit my mind lately to plan out my retirement plan. Well, it’s almost 20 years from now, and I think I need to start think about it.

As I walked daily to office, I had noticed that actually I’m forcing myself to go to the office. I was thinking, when my service is no longer required, am I gonna just sit at home, or shall I do something to earn?

Let’s say, from 55-80 years. Most of people are waiting for their employee fund or some pension. Well, I’ve been surrounded with elderly people who even had 1m of saving, however due to poor money management,, the guy need to live as poverty now coz the money is gone on all unnecessary things.

We really don’t know until when we gonna live. If you still alive until 90 yo, how will you manage your expenses during those days? What kind of expenses required? Are you gonna depend on your kids or will you do something to earn?

I think the major issue will be health and food, when we getting older. Food interm of food supplement and medicine. Most of famous diseases among Malaysian are high blood, diabetic melitus, cancer, heart attack and stroke. and another 1 more I was thinking was to make any will. Do I need to make a will, I’m still thinking on that as I had couple of property and funds to take care.

The other thing that trigger my mind. If we die, how about our social media. How do we deactivate all our social media accounts. I guess at least I need to list down how many are there? I need to set everything as preparation for the next life.

Well, I guess for me I will plan out to earn myself by the age of 50. Insya Allah.

For the past few months, I’ve been through a turbulent changes in my life. I’m started losing control of myself, my life and my surrounding. It’s a perfect time to slowing down all of the issues and take one by one step to solve it. To get back incharge of my ownself. So, here my longterm goal to achieve before entering Year 2023. Risk to be taken on each of stages, and consequences of each steps taken.

1. Financial base

To list down all monthly budget and to open relevant accounts for a long term savings goal. To track payment on each items such as Insurance, House payment, Credit Card payment etc.

2. Personal relationship

To put on hold for any toxic relationship or anything might leads for fights. I have tired of relationship, as you need to give some extra effort for them. For now, I will just put it on hold, and will check again if it’s really required to have any relationship or not. The risk assessment for a longterm goal will need to resume after the rest of item completed.

3. Work focus on longterm goal achievement

I guess, I had found a good environment workplace, yes it was. Unfortunately, it doesn’t gimme some sort of flexibility in a long run. So, I will need to find a good workplace environment with good colleague, and at the same time gimme some flexibility hours to sort my schedule. I’m loooking for work from home kind of company, so I balance out my life.

4. Family matters

Something that I’m trying to sort now. To make more time with family, to hangout and incharge on family matters. I’m kinda slighly off for pass few months, now it’s time to get incharge with them and spending more time with them.

5. Innerpeace Activities

Recently, I just figure out the company I work now having Zumba classes twice a week, I will start with that first. Later on, I think I will try to resume either my muaythai training or belly dance. Let’s see how.

So, okay. Those 5 things i need to sort before entering year 2023. I hope I can sort it, insya Allah 🙂

Hello everyone!!! It’s been awhile I’m away from blog! Haha..so, here we go. Let’s start with financial planning for year 2023..hahaahaha..yes…for 2023!! Let’s plan for future! LOL

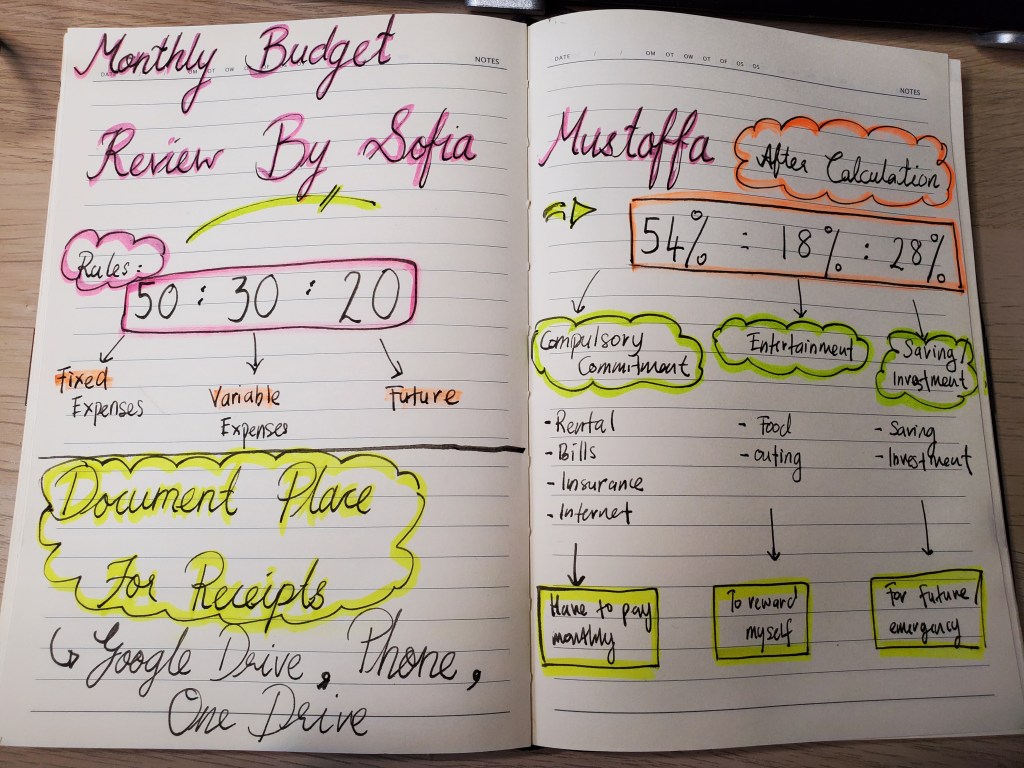

Okay, I’d checked on whatever resource I have, google, youtube…etc. So, I found the rules 50:30:20. It’s kinda interesting to check on. So, I made some calculation and hey yaa!!! I managed to get more savings! Yay!!! Way to go…minimalist lifestyle 🥳🥳

Monthly Budget follow rules 50:30:20 …

For rules 50:30:20, this is the percentage that you need to allocate your monthly income. There are 3 categories, the 50% should be the Fixed Expenses that you will need to pay such as bills, rental, car, internet, tuition fee etc (compulsory to pay). For the 30% of your salary should go to Variable Expenses that you have options not to spend such as eating outside, movie, theme park, present, etc. The remaining 20% should go to your Future Plans such as emergency savings or any possible investment. Well, after the calculation, I had found out that my Fixed Expenses is 54%(slightly higher because I included insurance with investment under this category 😄), my Variable Expenses is 18%(I dont have much things to buy, just lil bit entertainment like movie/eating outside) and for Future plans I have 28% 😃. I think this is good enough. As a minimalist, I always conscious on what to buy so that I don’t waste my money for clutters 😃

Okay, how do I calculate all of these? Haha..im using a simple ratio calculation 😜

Let’s take example, income salary RM2000 and to follow rules 50:30:20 (%).

In this example, when you calculate all your bills (plus other compulsory to pay) and it total up for example RM 900. So, a simple ratio (900/2000) x 100 = 45%. So for those who has salary RM2000, how to calculate is to manage the Fixed Expenses below RM 1000, RM 600 for Variable Expenses and RM 400 for Future plans. 😃

Where to store your monthly receipts for Tax Relief ?

Okay, I usually save in cloud, so easier to trace it. So, Im using Google Drive most of the times. Perhaps, you can have some other storage as well like One Drive. It is not really advisable to store in phone, as Phone can easily spoil then you will need to factory reset and all will be gone.

Okay, next I’m gonna explore how to diversify the savings and investments..till then..to be continue…